Durbin and Koopman: Box-Jenkins Examples¶

See Durbin and Koopman (2012), Chapter 8.4

%matplotlib inline

import numpy as np

import pandas as pd

from dismalpy import ssm

import matplotlib.pyplot as plt

# Get the basic series

dinternet = np.array(pd.read_csv('data/internet.csv').diff()[1:])

# Remove datapoints

missing = np.r_[6,16,26,36,46,56,66,72,73,74,75,76,86,96]-1

dinternet[missing] = np.nan

# Statespace

mod = ssm.SARIMAX(dinternet, order=(1,0,1))

res = mod.fit()

print res.summary()

Statespace Model Results

==============================================================================

Dep. Variable: y No. Observations: 99

Model: SARIMAX(1, 0, 1) Log Likelihood -225.770

Date: Mon, 21 Sep 2015 AIC 457.541

Time: 14:49:44 BIC 465.326

Sample: 0 HQIC 460.691

- 99

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.6562 0.092 7.156 0.000 0.476 0.836

ma.L1 0.4878 0.111 4.394 0.000 0.270 0.705

sigma2 10.3402 1.569 6.590 0.000 7.265 13.416

===================================================================================

Ljung-Box (Q): nan Jarque-Bera (JB): nan

Prob(Q): nan Prob(JB): nan

Heteroskedasticity (H): nan Skew: nan

Prob(H) (two-sided): nan Kurtosis: nan

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients.

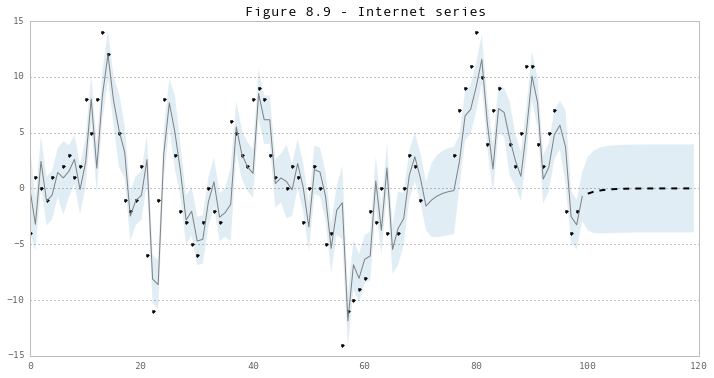

# In-sample one-step-ahead predictions, and out-of-sample forecasts

nforecast = 20

predict = res.get_prediction(end=mod.nobs + nforecast)

idx = np.arange(len(predict.predicted_mean))

predict_ci = predict.conf_int(alpha=0.5)

# Graph

fig, ax = plt.subplots(figsize=(12,6))

ax.xaxis.grid()

ax.plot(dinternet, 'k.')

# Plot

ax.plot(idx[:-nforecast], predict.predicted_mean[:-nforecast], 'gray')

ax.plot(idx[-nforecast:], predict.predicted_mean[-nforecast:], 'k--', linestyle='--', linewidth=2)

ax.fill_between(idx, predict_ci[:, 0], predict_ci[:, 1], alpha=0.15)

ax.set(title='Figure 8.9 - Internet series');